Your Canadian Retirement Plan, Made Simple.

Take total control of your financial future. Use powerful AI tools to optimize your tax strategy, plan your spending phases, and maximize your after-tax estate.

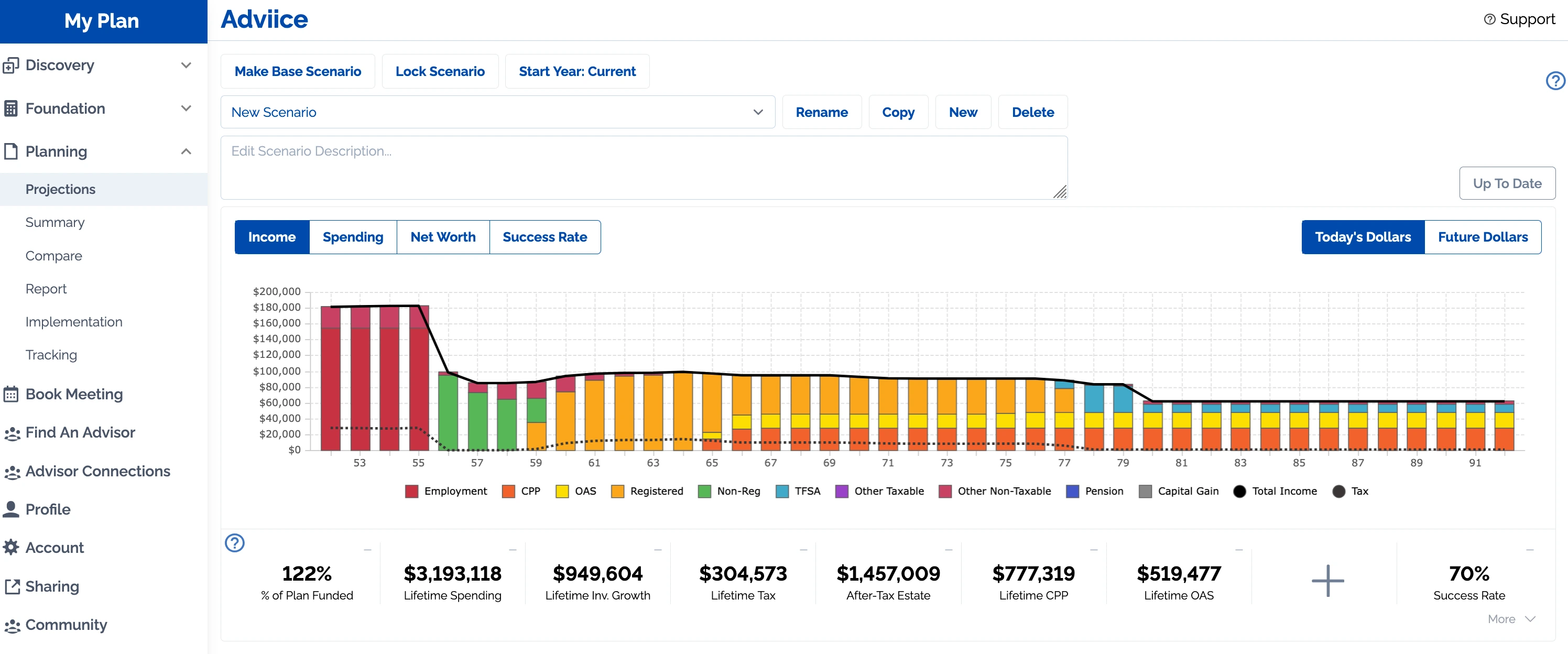

Platform highlights

- Spend More

- Melt Down Your RRSP

- Track Your Progress

- Maximize CPP & OAS

- Pay Less Tax

- AI-Powered Optimization

Boost Your Retirement

As Certified Financial Planners who helped 1,000+ Canadians plan better retirements, we wanted to make expert retirement planning easier and more accessible. That is why we built Adviice.

In this video, we build a newly retired couple's plan in 15 minutes. By mapping out a tax-efficient withdrawal strategy and phasing their spending, we:

- Boost their plan's success rate from 68% to 95%

- Add $50,000+ to their after-tax estate value

- Unlock an extra $30,000 a year for early retirement spending

Stop guessing and start planning with Adviice.

Adviice on YouTube Over 1M views · 140+ videos on retirement planningProfessional-Level Financial Planning, Accessible to Everyone

No matter how complex your financial situation, Adviice offers the tools and features you need to plan with confidence.

Taxes

Federal and all provinces included

Spending

Recurring, spending phases (Go-Go, Slow-Go, No-Go) and one-time purchases

Investment Draws

Mix draws from multiple account types: RRSP, LIRA, TFSA, FHSA, ESPP and more

Corporations

Add multiple Hold/Op corps

Real Estate & Rental

Future purchases, sales, and multiple rental properties managed separately

Government Benefits

Estimate CPP and OAS while dynamically adding other federal/provincial benefits you may qualify for

Debt

Mortgages, HELOCs, and investment loans

Stress Test

See how your plan performs in 100+ historical sequences

Compare

Build multiple scenarios and see how they match up

Real Canadians. Real results.

Go from uncertainty to confidence

Stop guessing whether you'll have enough. Adviice runs the numbers on CPP timing, tax strategies, and drawdown sequences — so you can see exactly where you stand.

“You can go from "I think we'll be ok" to full confidence in your plan, based on real data and all the calculations it does for you.”

AI strategies that actually make sense

Our AI doesn't just crunch numbers — it explains its reasoning. Explore well-reasoned strategies for tax optimization, CPP/OAS timing, and RRSP meltdowns, all in plain language.

“The entire Adviice package is absolutely outstanding. Their AI strategies are well-reasoned and make exploration simple.”

A comprehensive plan, not a calculator

Adviice builds a year-by-year withdrawal plan across all your accounts — RRSP, TFSA, non-registered — optimized to minimize lifetime taxes.

“The plan generated is comprehensive with yearly withdrawals from different sources to optimize paying taxes. I will certainly recommend you to others.”

Powerful tools, simple interface

CPP/OAS integration, AI recommendations, success rate modelling, and manual overrides — all in a clean, user-friendly interface. Built by CFPs, designed for everyone.

“The user interface is simple and user-friendly. I love the CPP/OAS integration, the AI recommendations, the success rate modelling… so many things to love.”

Simple, transparent pricing

Everything you need — at an affordable price.

Your Confident Retirement Starts Here

Affordable, easy-to-understand planning for everyday Canadians. Cancel anytime.

Start PlanningCommon retirement questions

These are the questions keeping Canadians up at night — and the ones Adviice was built to answer.

When should I start CPP?

The optimal CPP start age depends on your health, other income sources, and how long you expect to live. Starting later (up to age 70) increases your monthly payment by 8.4% per year after 65, but you miss years of payments. Adviice models hundreds of scenarios to find the CPP start age that maximizes your lifetime income.

When should I start OAS?

Like CPP, you can defer OAS from age 65 up to 70 for a 7.2% annual increase. But OAS has a clawback that kicks in at higher income levels, so the best timing depends on your full retirement income picture. Adviice factors in OAS clawback, GIS eligibility, and tax interactions automatically.

How much can I safely spend in retirement?

There’s no single “safe” number — it depends on your savings, CPP/OAS timing, tax situation, and how long your money needs to last. Adviice runs Monte Carlo simulations across hundreds of market scenarios to show you a spending level that balances comfort with sustainability.

Will I run out of money?

That’s the question that keeps most pre-retirees up at night. The answer depends on your withdrawal strategy, investment returns, and how long you live. Adviice gives you a success rate — the percentage of scenarios where your money lasts your entire retirement — so you can plan with confidence, not guesswork.

How can I pay less tax in retirement?

Strategic withdrawal sequencing (which accounts to draw from and when), RRSP meltdown strategies, and pension income splitting can significantly reduce your lifetime tax bill. Adviice’s AI evaluates tax-optimized drawdown sequences automatically as part of your plan.

Which accounts should I draw from first?

The conventional wisdom of “TFSA last” isn’t always right — the optimal drawdown order depends on your marginal tax rate in each year of retirement. Adviice models the tax impact of different withdrawal sequences across your RRSP, TFSA, and non-registered accounts to find the most efficient order.

When can I actually retire?

Your retirement date depends on the gap between your savings and your spending needs, adjusted for CPP, OAS, and investment returns. Adviice calculates the earliest date you can retire while maintaining your target spending with a high probability of success.

Am I going to be okay?

That’s exactly why we built Adviice. Instead of wondering, you can see a clear picture: your projected income, your success rate, and the specific strategies that improve your outcome. Over 10,000 Canadians have already used Adviice to answer that question.